The age of your roof changes everything about how your homeowners insurance responds to a claim. This complete guide explains exactly what San Antonio insurers look for on a 15-year-old roof, what they will and will not pay, and how to protect yourself before the next hailstorm hits.

If your San Antonio home has a roof that is around 15 years old, you are at one of the most important thresholds in residential roofing insurance. Below that age, most homeowners policies treat storm damage as a full replacement cost event. At or beyond that age, the picture changes significantly depending on your policy type, your carrier, and the condition of the roof at the time of the loss.

The honest answer to whether insurance will cover your 15-year-old roof is: it depends on four things. The type of policy you hold, the cause of the damage, the condition of the roof before the storm, and how your claim is documented and filed. This guide walks through every one of those factors so you can go into a claim conversation with your carrier informed, prepared, and protected.

Age alone does not determine whether your claim is covered. Cause of damage does. Homeowners insurance in Texas covers sudden, accidental losses caused by events like hail, wind, and falling trees. It does not cover gradual deterioration, wear and tear, or damage that existed before your policy was in force. A 15-year-old roof damaged by a hailstorm last Tuesday is a covered claim. A 15-year-old roof that has been leaking slowly for two years is not. Understanding that distinction is the foundation of every insurance decision you make about your roof.

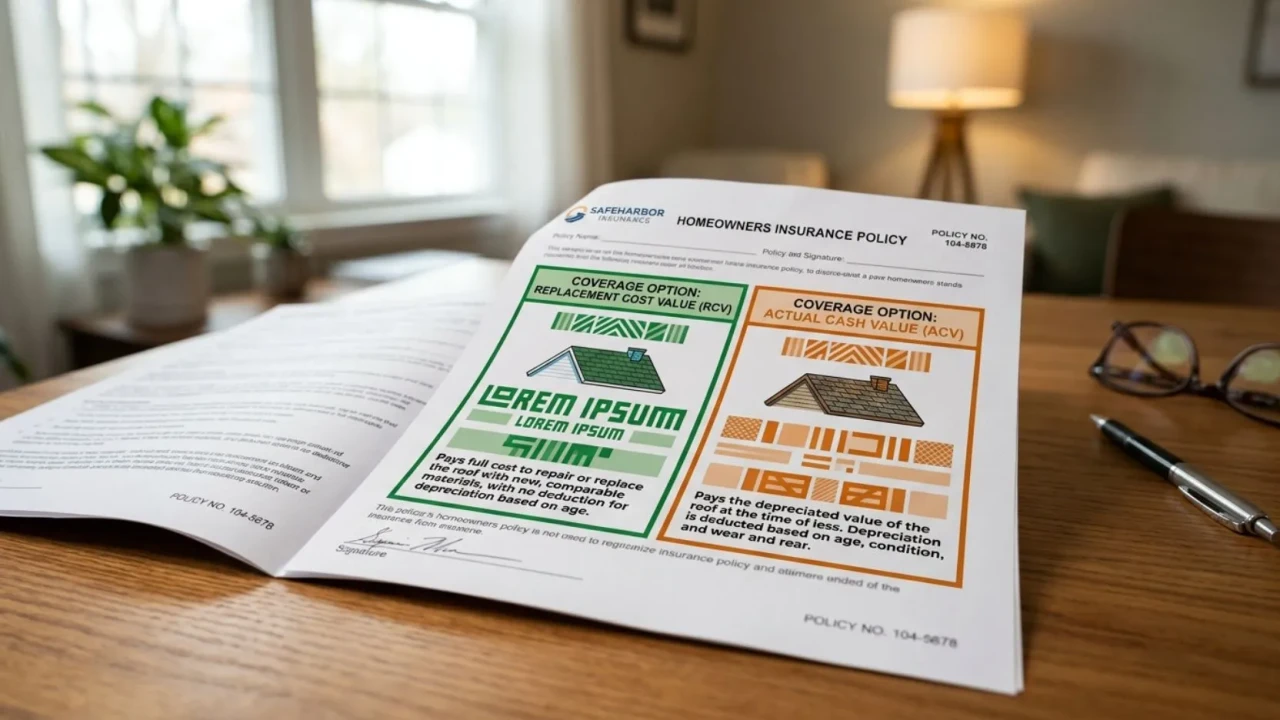

The most consequential variable in any older roof insurance claim is whether your policy pays on a Replacement Cost Value basis or an Actual Cash Value basis. Most San Antonio homeowners do not know which one they have until they file a claim, and by then it is too late to change it. Reading this before you have a claim is the most valuable thing you can do for your financial protection.

Replacement Cost Value (RCV): Your insurer pays the full cost to replace your damaged roof with materials of like kind and quality at today's prices, minus your deductible. This is the policy type you want. On a 15-year-old roof destroyed by hail, RCV coverage means the insurance company funds a new roof regardless of how old the original one was. Some Texas carriers have begun limiting RCV coverage on roofs over a certain age, so confirm this with your agent directly.

Actual Cash Value (ACV): Your insurer pays the depreciated value of the roof at the time of the loss. On a 15-year-old asphalt shingle roof with an expected lifespan of 20 to 25 years, that depreciation can reduce your payout by 40 to 60 percent. If a new roof costs $18,000 and the insurer applies 50 percent depreciation, your check before the deductible is $9,000. You cover the rest out of pocket.

- Confirm whether your roof is covered at RCV or ACV on your current declarations page

- Ask your agent whether your carrier applies age-based depreciation schedules regardless of policy type

- Check whether your RCV policy has a "functional replacement cost" clause that limits payout to a lesser material

- Confirm your wind and hail deductible amount, which in San Antonio is often a percentage of home value, not a flat dollar figure

- Ask whether depreciation is recoverable after the work is completed, or whether it is withheld permanently

- Review your policy annually at renewal, as carriers sometimes downgrade coverage terms without a prominent notice

Texas homeowners insurance is a sudden-loss product. It is designed to respond to unexpected events that cause damage in a short period of time. What it is not designed to cover is the slow, predictable decline of a material over its service life. The distinction between those two categories decides whether your claim gets paid or denied, and it is where most homeowners get surprised.

On a 15-year-old asphalt shingle roof, the practical challenge is that some storm damage genuinely looks like age-related wear to an untrained eye, and some legitimate wear gets misidentified as storm damage by contractors looking for an easy claim. A qualified roof inspection by a licensed contractor before you file a claim is the best way to understand exactly what you have and what category it falls into. Filing a claim for damage that an adjuster categorizes as wear-and-tear results in a denial, and that denial goes on your claims history regardless of the outcome.

Under Texas law, you have one year from the date of the storm or damage event to file a claim under most homeowners policies. After major hail events in San Antonio, some homeowners wait too long and lose the right to file. If you suspect your roof sustained storm damage, have it inspected by a licensed roofing contractor within 30 days of the event, even if you do not see any interior signs of a leak yet. Hail and wind damage on a 15-year-old shingle roof can be significant and invisible from the ground, and the clock on your filing window starts the day the storm hits, not the day you notice a drip.

- Note the exact date of the storm event and save any weather service records confirming hail size and track

- Take photos of any visible damage from the ground immediately after the storm

- Do not have anyone walk the roof until a licensed contractor can assess it safely

- Get a written inspection report from a licensed San Antonio roofing contractor before calling your insurer

- Keep records of any emergency repairs made to prevent further damage, as these costs are typically reimbursable

- File the claim promptly, well within the one-year Texas window, and note the claim number for all future correspondence

When an adjuster inspects your storm-damaged roof, they are doing two things at the same time. They are assessing the storm damage, and they are assessing the pre-existing condition of the roof. On a 15-year-old asphalt shingle roof, these two assessments are deeply intertwined. A roof in poor pre-storm condition gives the adjuster grounds to attribute more of the damage to wear rather than the storm event, which reduces the claim payout or supports a denial.

This is why regular maintenance on an aging San Antonio roof is not just good practice from a durability standpoint. It is documentation. A roof that has been maintained, inspected, and repaired as needed creates a condition baseline that supports your position in a claim. A roof that has been ignored for five years gives the adjuster tools to use against you.

What adjusters look for in pre-storm condition: Significant granule loss across the field of the roof, curling or cupping shingle edges, cracked or missing shingles, moss or algae growth indicating chronic moisture, lifted or improperly sealed flashings, and any evidence of prior leaks that were not repaired. Each of these items gives the adjuster a basis to attribute a portion of the loss to pre-existing deterioration rather than the storm.

How maintenance documentation protects you: If you have records of inspections, minor repairs, and maintenance performed on your roof in the years before the storm, you have evidence that the pre-storm condition was acceptable. A licensed contractor's signed inspection report from two years ago noting a sound roof is worth more in a claim dispute than any argument you can make after the fact.

Request a pre-claim inspection from a licensed San Antonio roofing contractor before the next hail season, not after a storm. A written inspection report documenting the current condition of your 15-year-old roof creates a formal baseline. If a storm hits six months later and the adjuster tries to attribute damage to pre-existing wear, your dated inspection report directly contradicts that position. It costs nothing to ask for this documentation, and it can be the difference between a full payout and a significant out-of-pocket expense after the next major storm.

- Schedule a professional roof inspection and request a written condition report for your files

- Address any minor repairs identified in the inspection before the next storm season

- Clear gutters and downspouts to eliminate moisture accumulation evidence that adjusters flag

- Document any moss, algae, or standing water issues and have them treated professionally

- Keep all invoices and work orders from any roofing contractor who has worked on your roof

- Photograph your roof from the ground annually as a baseline record with a date stamp

Filing a roof insurance claim on a 15-year-old San Antonio home is a process where the sequence matters. Homeowners who call their insurer before understanding what they have often frame the claim incorrectly. Homeowners who have a contractor inspect and document the roof first go into the claim conversation with evidence, not just a complaint. Here is the correct sequence.

- Storm date documented with weather service records before the claim is opened

- Licensed contractor inspection completed and written report received before calling the insurer

- Claim filed with the carrier within the Texas one-year filing window, well in advance of the deadline

- Claim number obtained and saved with all claim correspondence

- Contractor scheduled to be present during the adjuster's roof inspection

- Adjuster's written scope of loss reviewed line by line against contractor's estimate

- No Assignment of Benefits document signed without reading it fully and consulting an attorney if needed

Not every 15-year-old roof claim in San Antonio ends in a full settlement. Understanding the most common reasons claims are denied or underpaid, and knowing what recourse exists, is as important as knowing how to file correctly in the first place.

| Reason for denial or underpayment | What it means | Your options |

|---|---|---|

| Damage classified as wear and tear | Adjuster attributes loss to age, not storm event | Request a second inspection with your contractor present; escalate to appraisal if disagreement persists |

| ACV policy with high depreciation | Insurer applies large age-based deduction before paying | Verify depreciation schedule is accurate for your shingle type; consider supplementing with a personal loan or financing |

| Claim filed outside the one-year Texas window | Policy deadline has passed | Consult a Texas insurance attorney; limited options remain at this stage |

| Cosmetic-only damage finding | Carrier acknowledges hail hit the roof but denies functional damage | Review policy language for cosmetic exclusions; consult a public adjuster or insurance attorney |

| Pre-existing damage exclusion | Adjuster finds damage predates the storm or the policy period | Counter with maintenance records and prior inspection reports showing acceptable condition |

| Scope dispute: adjuster proposes repair, contractor recommends replacement | Disagreement on extent of loss | Invoke the policy's appraisal clause; each party appoints an appraiser, and a neutral umpire resolves the dispute |

Texas has strong consumer protection laws that govern how insurance companies handle claims. Carriers have statutory deadlines to acknowledge a claim, investigate it, and either pay or deny it. Unreasonable delays or bad-faith handling can expose a carrier to additional liability under the Texas Insurance Code. If you believe your claim has been handled improperly, a Texas-licensed public adjuster or a property insurance attorney can review your situation at little or no upfront cost, as many work on contingency.

- Request the denial or underpayment explanation in writing from your carrier immediately

- Get a second independent inspection from a different licensed San Antonio roofing contractor

- Review your policy's appraisal clause, which provides a formal dispute mechanism most homeowners never use

- Consult a licensed Texas public adjuster if the disputed amount exceeds $5,000

- Contact the Texas Department of Insurance to file a complaint if you believe the carrier acted in bad faith

- Consult a Texas property insurance attorney, many of whom offer free initial consultations for denied roof claims

Use this table to understand how different policy types and scenarios play out on an aging roof in the San Antonio market. All figures are illustrative and based on typical 2026 San Antonio conditions. Your specific outcome depends on your policy language, carrier, and documented loss.

| Scenario | Policy type | Likely outcome | Homeowner cost exposure |

|---|---|---|---|

| Hail damage, well-maintained roof, RCV policy | Replacement Cost Value | Full replacement funded by insurer | Deductible only (typically $1,000 to $3,000) |

| Hail damage, well-maintained roof, ACV policy | Actual Cash Value | Partial payment after 40 to 60% depreciation | Deductible plus $6,000 to $11,000+ out of pocket on a typical home |

| Wind damage, one area of lifted shingles, RCV | Replacement Cost Value | Repair or partial replacement covered | Deductible only if damage exceeds the deductible threshold |

| Granule loss, curling shingles, no storm | Any policy | Denied as wear and tear | Full replacement cost out of pocket |

| Slow leak, deferred maintenance | Any policy | Denied as maintenance issue | Repair plus any interior water damage out of pocket |

| Hail damage, neglected roof, ACV policy | Actual Cash Value | Partial payment with heavy depreciation; pre-existing condition disputes likely | Large out-of-pocket exposure; possible partial denial |

| Tree falls on roof from storm | Any standard policy | Covered as sudden accidental loss | Deductible only under most Texas policies |

- Pull your declarations page and confirm whether your roof is covered at RCV or ACV

- Confirm your wind and hail deductible, which in San Antonio is commonly 1 to 2 percent of your home's insured value

- Ask your agent whether your carrier applies an age-based coverage restriction or schedule for roofs over 15 years

- Schedule a professional inspection and request a written condition report for your records

- Complete any recommended minor repairs before storm season to protect your pre-storm condition baseline

- Photograph your roof from the ground with a date-stamped image each spring

- Document the storm date and save any weather service records confirming hail size over your specific neighborhood

- Photograph any visible damage from the ground before anyone walks the roof

- Call a licensed San Antonio roofing contractor for a free post-storm inspection

- Obtain a written contractor inspection report before opening a claim with your insurer

- Make any emergency temporary repairs needed to prevent further damage and save the invoices

- Do not sign any AOB or Assignment of Benefits document from a contractor or third party

- File the claim within the Texas one-year window, well before the deadline, with your storm documentation ready

- Request that your roofing contractor be present during the adjuster's roof inspection

- Obtain the adjuster's written scope of loss and compare it line by line with your contractor's estimate

- Request any denial or underpayment explanation in writing from the carrier

- Invoke the appraisal clause in your policy if the scope dispute cannot be resolved with the adjuster directly

- Consult a licensed Texas public adjuster or property insurance attorney if the denied or underpaid amount is significant

Get a free roof inspection before you file a claim

If your San Antonio home has a 15-year-old roof and there has been a recent storm in your area, call us before you call your insurer. We will inspect your roof for free, document what we find in writing, and walk you through exactly what you have before you open a claim.